Why a lump-sum sale is so expensive

Consider a California retiree selling a long-held rental property: $300,000 cost basis, $1,800,000 sale price, $1,500,000 capital gain. Conventional sale, all recognized in one year.

The tax stack on that $1.5M gain in 2026:

- Federal long-term capital gains: Some at 15%, some at 20% once you cross the $613,700 MFJ taxable income threshold. Net effective ~17-19% federal LTCG on the gain. Roughly $275-300K.

- Federal Net Investment Income Tax (NIIT): 3.8% surtax on the gain above the $250K MFJ MAGI threshold. Roughly $57K.

- California state tax: CA taxes capital gains as ordinary income — no preferential rate. The top CA bracket of 13.3% kicks in fast on a $1.5M gain. Effective state tax ~13% on most of it. Roughly $195-200K.

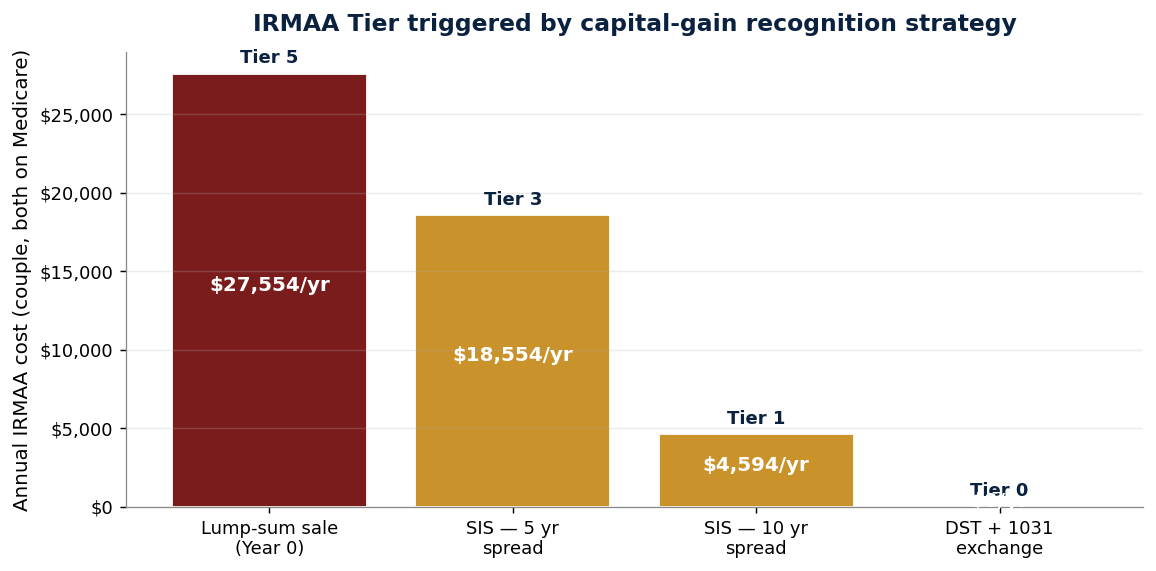

- IRMAA spike (2 years later): The $1.5M+ MAGI puts you firmly in IRMAA Tier 5 for the year. A couple both on Medicare pays roughly $27,554 of extra Medicare premium for that one year.

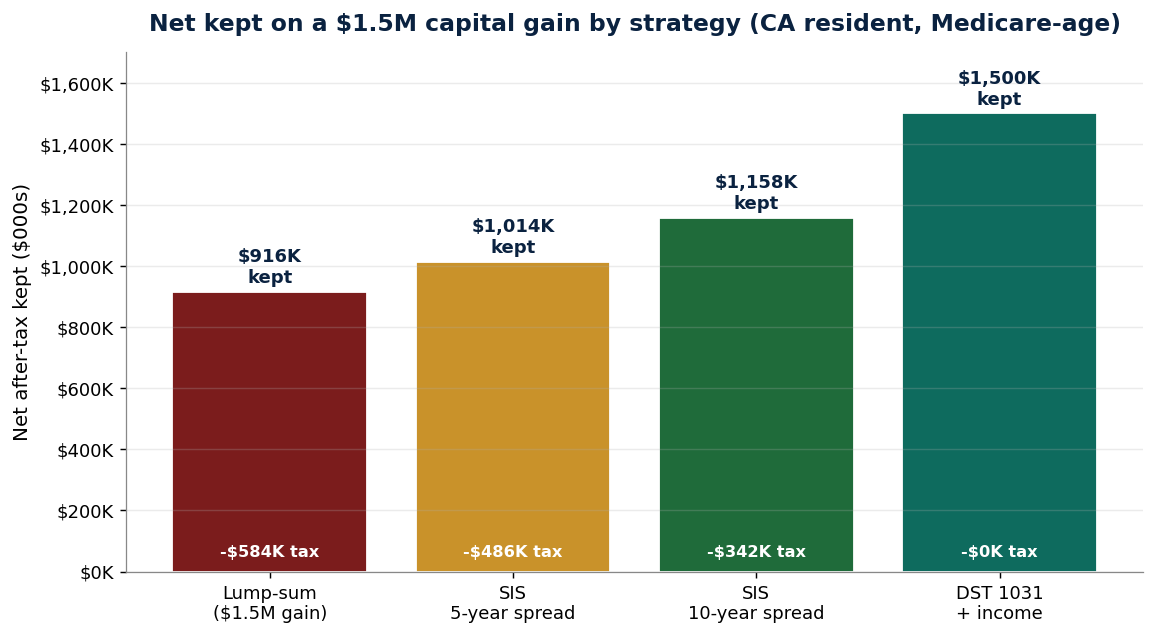

Combined tax + IRMAA bill: roughly $560,000-$585,000 on a $1,500,000 gain. The retiree keeps about 61% of the appreciation.

This is what we'll call the "tax bomb" baseline. Every strategy below measures itself against this number.

The Structured Installment Sale (Section 453)

Section 453 of the Internal Revenue Code is a 100+ year-old provision that allows sellers of property to recognize the capital gain as the payments are received, rather than all at once at closing.

The classic seller-financed installment sale (Mom-and-Pop holds a note for the buyer) qualifies under Section 453 — but it requires the seller to take on credit risk and asset-management duties for years or decades. Most sellers don't want that.

The Structured Installment Sale (SIS) solves this. The buyer pays cash at closing. The cash goes to a third-party "assignment company" (typically an insurance company-affiliated entity). The assignment company then pays the seller on a customized fixed schedule — say $300,000/year for 5 years, or $150,000/year for 10 years, or whatever the seller chooses. The schedule is guaranteed and not subject to buyer creditworthiness.

From the seller's tax perspective: the gain is recognized as the payments arrive, prorated against the cost basis. From the buyer's perspective: it's a normal cash sale.

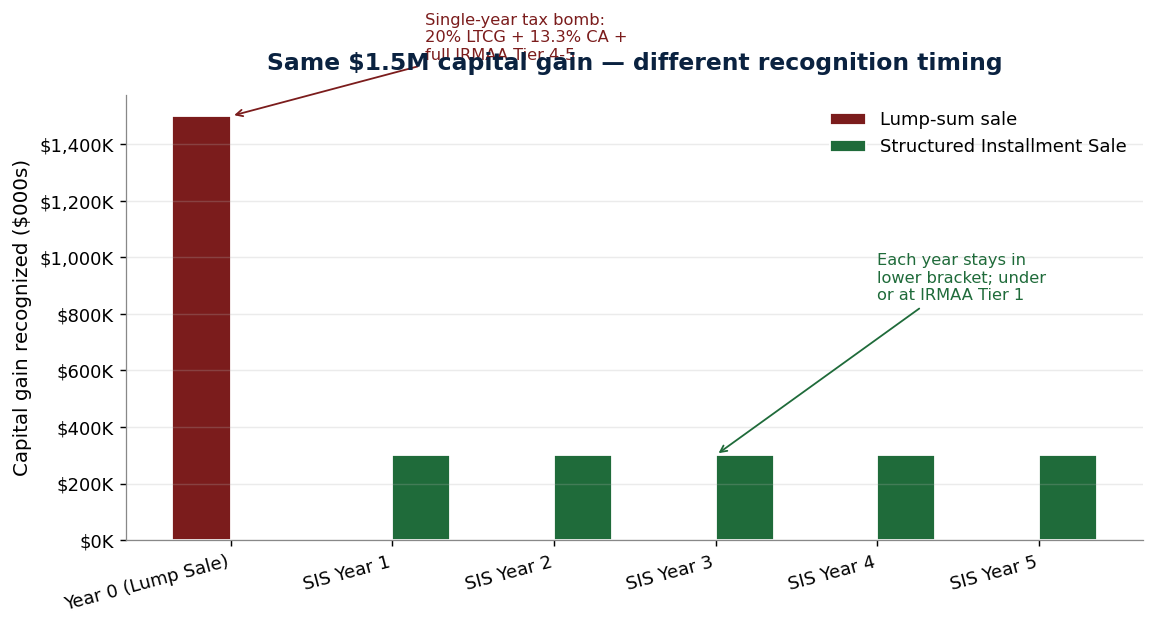

The 5-year SIS spread keeps annual capital gain recognition at $300K instead of $1.5M. That single change ripples through every other tax decision: lower brackets, lower NIIT exposure, lower IRMAA tier, lower state tax bracket.

How SIS interacts with IRMAA

The IRMAA interaction is one of the most undersold benefits of the SIS. A $1.5M gain recognized all at once puts a Medicare-age couple firmly in IRMAA Tier 5 for that year, costing roughly $27,554 of extra Medicare premium.

A 5-year SIS that spreads the gain into $300K annual recognitions stays in IRMAA Tier 3 — about $9,277/year extra. Over 5 years that's about $46,385.

A 10-year SIS at $150K annual recognition stays in IRMAA Tier 1 — about $2,297/year extra. Over 10 years that's about $22,970.

A DST (next section) defers the recognition entirely — IRMAA stays at baseline.

For Medicare-age sellers, the IRMAA interaction alone can shift the optimal strategy. A 10-year SIS that costs more in cumulative IRMAA than a 5-year SIS could still win on total after-tax wealth because the federal + state brackets stay lower.

The Delaware Statutory Trust (DST) and 1031 exchange

The 1031 exchange (Section 1031) lets you defer all capital gain by reinvesting sale proceeds into another "like-kind" real estate property within strict timelines (45 days to identify, 180 days to close). For real estate-to-real estate exchanges, this works well — but most retirees don't want to actively manage a new property.

The Delaware Statutory Trust solves this. A DST is a passive ownership structure that holds institutional-grade commercial real estate (apartments, industrial, medical office, single-tenant net-lease properties, etc.). You exchange into a fractional ownership of the DST. The DST sponsor manages the property. You receive monthly distributions and depreciation pass-through. No active management on your part.

The result: you defer the entire $1.5M capital gain. Your cost basis carries over into the DST shares. You collect income from the DST. When you eventually die holding the DST, your heirs receive a full step-up in basis — meaning the deferred gain disappears entirely.

DSTs aren't free. They have sponsor fees, less liquidity than direct ownership, and exposure to commercial real estate market risk. But for retirees looking to exit hands-on landlording without triggering a tax bomb AND maintain real estate income, the DST is a clean exit.

Total after-tax wealth comparison

Same $1.5M capital gain. Same CA-resident retiree on Medicare. Four strategies. Total after-tax dollars kept:

The lump-sum sale keeps about $915K of the $1.5M (61%). The 5-year SIS keeps roughly $1.01M (67%). The 10-year SIS keeps about $1.16M (77%). The DST defers the entire $1.5M and steps up at death — meaning the heirs receive the full gain tax-free.

The DST strategy depends critically on actually holding the position until death. If the seller has to sell DST shares later (unforeseen liquidity need), the deferred gain comes due at that point. For retirees with a clear "hold to step-up" plan, DST is the most powerful tool. For retirees who may want flexibility, the 10-year SIS often wins.

When each strategy is the right fit

The right tool depends on the seller's situation:

Lump-sum sale

- Small gains where the spread benefit is small

- Seller is in the 0% LTCG bracket (taxable income under $98,900 MFJ)

- Seller needs all proceeds immediately for another purpose

Structured Installment Sale (Section 453)

- Gain is $500K+ — large enough that spreading matters

- Seller wants the cash spread out as income (e.g., to replace earned income in retirement)

- Seller wants flexibility to take a fixed-schedule payment without managing real estate

- Seller is comfortable with a 5-10 year payment commitment from an insurance-company-backed assignment

DST 1031 Exchange

- Gain is substantial AND seller wants to maintain real estate exposure for income

- Seller plans to hold until death to capture step-up basis

- Seller is comfortable with commercial real estate market risk

- Seller wants to fully exit active landlording without active reinvestment

Hold to death (no sale)

- Seller doesn't need the liquidity

- Property is generating acceptable income

- Heirs will receive a full step-up in basis at death

- Often the cleanest answer when applicable

For California retirees with appreciated rental property, the most common right answer is "hold to death if you can, structured installment sale if you can't, DST if you want continued real estate income without active management." All three dramatically beat the lump-sum default.

What to actually do

If you have appreciated real estate you're considering selling, the priority list:

- Calculate your embedded gain. Current sale value minus cost basis (including depreciation recapture). Anything over $250K-$500K of gain warrants exploring SIS or DST.

- Decide your liquidity needs. Do you need the cash immediately for retirement income, a property purchase, or something else? Or could the cash arrive over 5-10 years as planned income?

- Map your post-sale tax bracket. What other income are you generating in the sale year — and the years following? This determines whether spreading helps and by how much.

- Get specific quotes. SIS assignment companies will quote you specific payment schedules and effective interest rates. DST sponsors will show you specific properties with current yields and projected returns. Compare quotes from multiple providers.

- Coordinate with your tax professional. Both SIS and DST have specific documentation and timing requirements. Mistakes here can void the tax treatment.

The workshop linked below walks through SIS and DST scenarios for common California real-estate-rich retiree situations.

Free workshop — Selling Appreciated Real Estate Without the Tax Bomb

Hans walks through Section 453 SIS and DST 1031 strategies in his SoCal workshops, with worked examples on real property values and CA-specific tax interactions.

See Upcoming Workshops