What OBBBA actually changed

OBBBA's biggest impact on retirees comes from five specific provisions:

- TCJA tax brackets made permanent. The seven-bracket structure (10/12/22/24/32/35/37%) was scheduled to sunset after 2025, reverting to pre-2018 brackets (15/28/31/36/39.6%). OBBBA made the TCJA structure permanent. No more 39.6% top bracket; the 37% top stays.

- Senior bonus deduction added. A new $6,000-per-spouse standard deduction add-on for filers age 65+, on top of the existing senior deduction. Phase-out begins at $75,000 MAGI Single / $150,000 MFJ and ends fully at $175,000 / $250,000. Sunsets after 2028.

- SALT cap raised to $40,400 (MFJ). The State and Local Tax deduction cap was raised from $10,000 to $40,400 for MFJ for 2026, with similar increases for other filing statuses. This phases down by income above certain thresholds and reverts to $10,000 in 2030.

- Estate exemption set permanently at $15M. The federal estate tax exclusion was scheduled to revert to roughly $7M per person in 2026. OBBBA raised it to $15M per person ($30M for couples with portability) and indexed it for inflation, made permanent.

- Section 199A QBI deduction made permanent. The 20% pass-through deduction, also scheduled to sunset, was made permanent. Important for retirees with consulting, rental real estate, or other pass-through income.

Combined, these provisions represent the largest single tax-cut continuity for retirees in recent memory. We'll walk through each one with charts.

The senior bonus deduction — the new big one for 65+

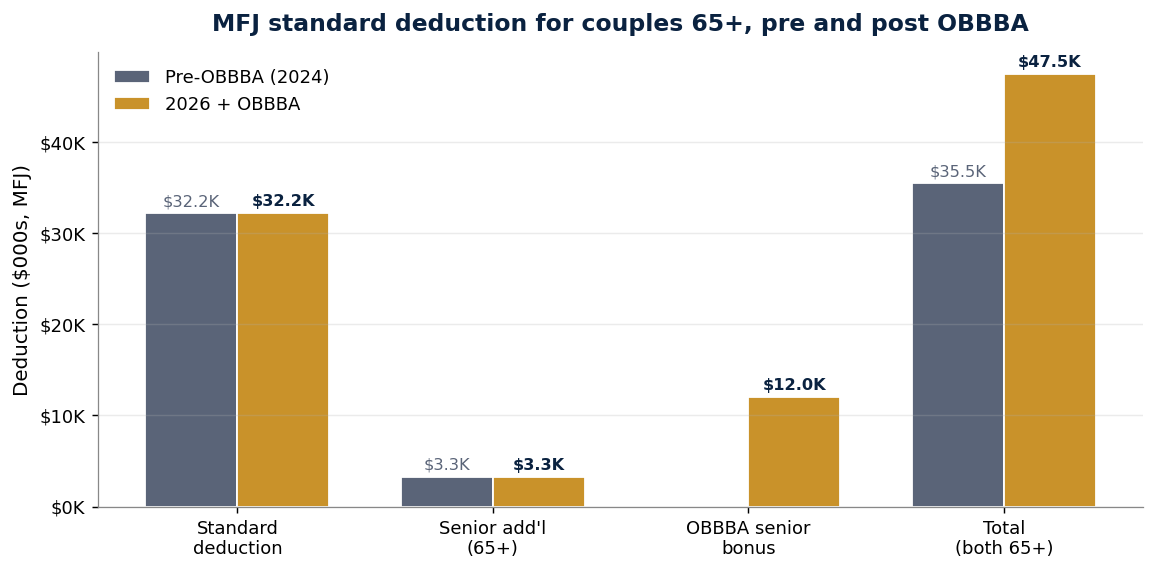

The senior bonus deduction is the most retiree-specific change in OBBBA. Each spouse age 65+ gets an additional $6,000 standard deduction. Both spouses 65+ = $12,000 of new MFJ deduction.

This stacks on top of the existing standard deduction ($32,200 MFJ in 2026) and the existing senior add-on ($1,650 per spouse 65+). For a couple both 65+, total standard deduction in 2026:

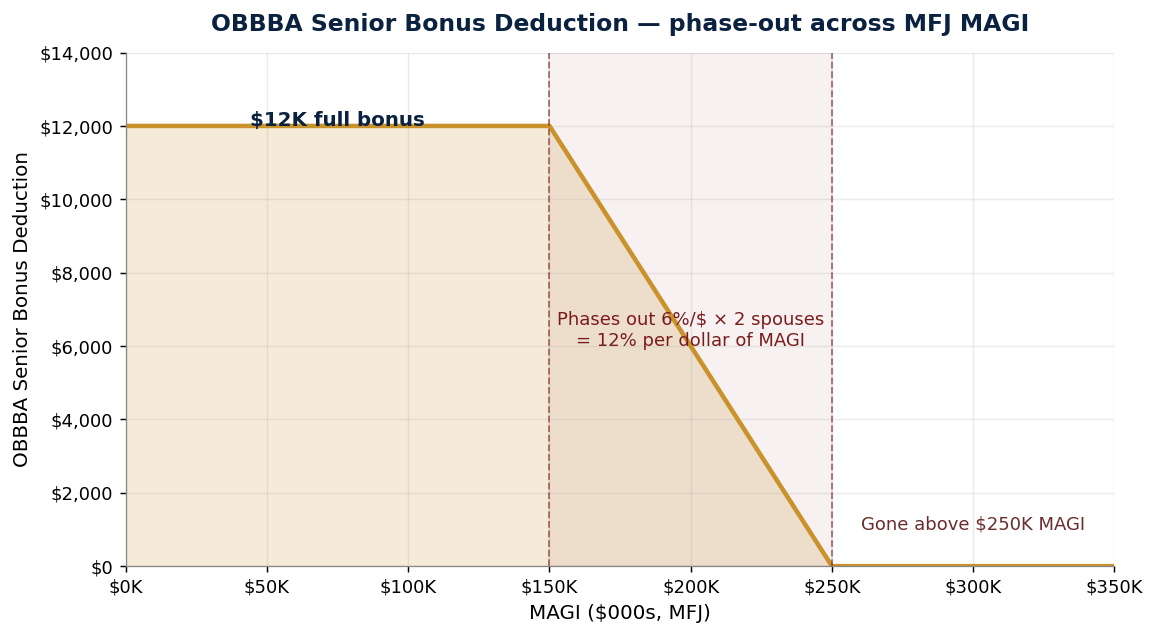

The $12,000 bonus phases out 6% per dollar of MAGI above $150,000 MFJ. Importantly, the phase-out applies per spouse, so for couples it's effectively 12% per dollar — meaning the bonus is fully gone by $250,000 MFJ MAGI.

Couples with MAGI under $150K capture the full $12,000. The middle-income retirees — between $150K and $250K MAGI — face the steepest effective marginal rate in U.S. retirement income tax history. Every additional dollar of MAGI in that range loses 12¢ of deduction. At a 22% federal marginal rate, that's an extra 2.64% effective rate on every dollar in the phase-out range. Stack that on top of the bracket rate, and the effective marginal rate in the phase-out zone can hit 27-28%.

What this means for federal tax owed

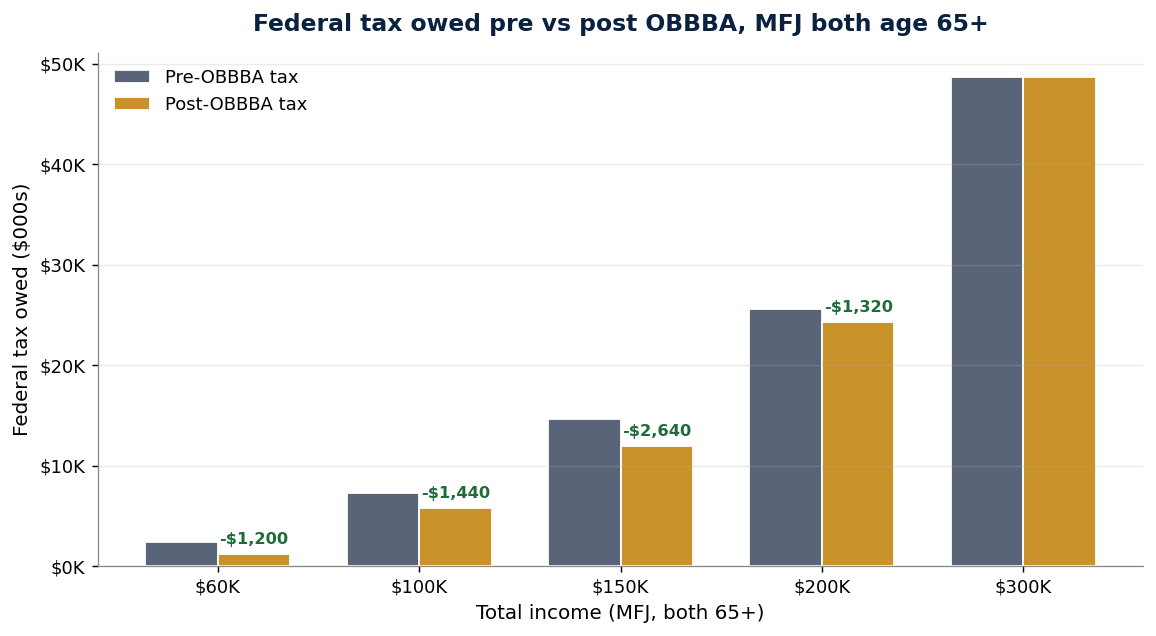

Comparing pre-OBBBA and post-OBBBA federal tax owed for an MFJ couple both 65+ at different income levels:

At $60K of total income, the couple saves roughly $1,400 in federal tax. At $100K, about $2,640. At $150K (right at the senior bonus phase-out edge), the savings peak at roughly $2,640. Above $150K the savings shrink rapidly as the senior bonus phases out. By $250K, the couple is back to the pre-OBBBA tax level (the bonus is fully phased out).

For middle-income retirees with total income $60K-$150K MFJ, OBBBA delivers $1,400-$2,640 of annual federal tax savings. For higher-income retirees, the senior-specific savings phase out quickly — but they still benefit from the permanent TCJA brackets, the larger SALT cap, and the permanent estate exemption.

The SALT cap change — relevant for many retirees

The TCJA originally capped the State and Local Tax (SALT) deduction at $10,000 for both Single and MFJ filers. This was particularly painful for high-tax-state residents (California, New York, New Jersey, etc.).

OBBBA raised the cap to $40,400 for MFJ filers in 2026 (and proportionally for other statuses), with phase-down provisions for very-high-income filers and a sunset in 2030 reverting to $10,000.

For California retirees:

- A couple owning a home with $15K of property tax + $20K of CA state income tax + $5K of registration fees = $40K of SALT. Under the old $10K cap, $30K of that was disallowed. Under the new $40,400 cap, the full $40K is deductible.

- Net federal tax savings at the 24% bracket: ~$7,200/year of additional itemized deduction × 24% = ~$1,728/year of federal tax saved.

- For retirees who weren't previously itemizing (because the old SALT cap kept their total itemized below the standard deduction), the new $40,400 cap can flip them into itemizing — potentially capturing another $10K-$20K of charitable + mortgage interest deductions that were previously wasted.

This is a meaningful planning shift for any CA, NY, NJ, MA, or similar high-tax-state retiree. The math says re-evaluate your itemize-vs-standard-deduct decision every year through 2029.

The estate exemption — the under-discussed big win

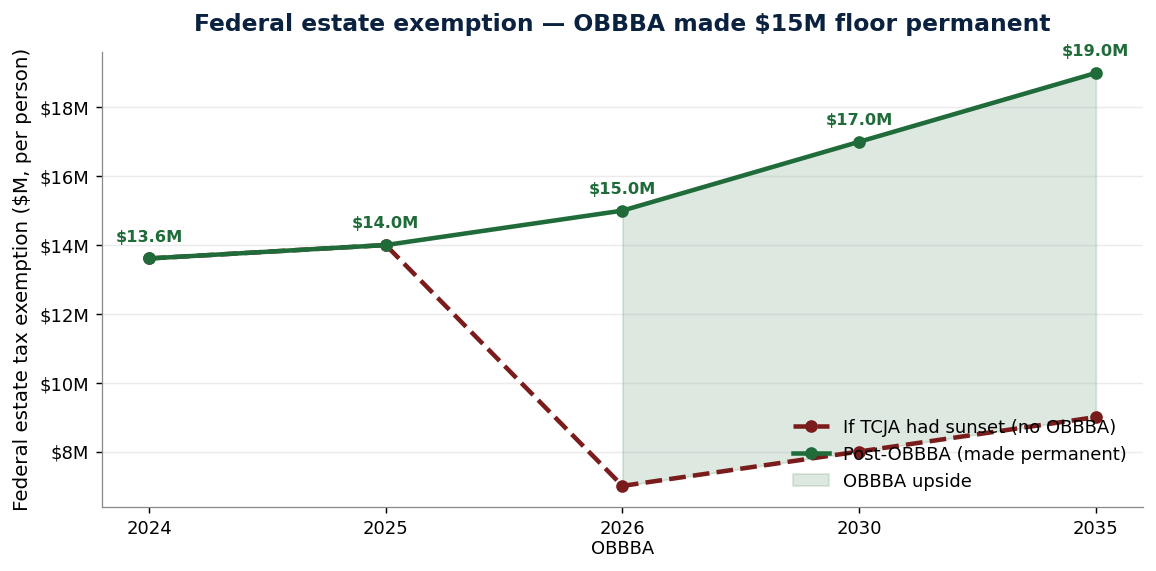

Under pre-OBBBA law, the federal estate tax exemption was scheduled to revert from ~$14M per person in 2025 to roughly $7M per person in 2026 (the pre-TCJA inflation-adjusted level). OBBBA reset the exemption to $15M per person, indexed for inflation, and made it permanent.

For a married couple using portability, the combined federal estate exemption is now $30M and indexed upward. This effectively removes federal estate tax exposure for the vast majority of American families. Less than 0.05% of estates will face federal estate tax under the OBBBA permanence.

Planning implications:

- Lifetime gifting strategies become less urgent for estates under $30M. The "use it or lose it" pressure from the scheduled 2026 sunset has been removed.

- Irrevocable life insurance trusts (ILITs) become more focused on liquidity and asset protection rather than estate tax minimization for most families.

- The income-tax-focused estate planning becomes dominant. Inherited IRA 10-year rules, step-up basis on brokerage, and Roth conversion timing matter more than federal estate tax minimization for most retirees.

- State estate tax planning still matters in 12+ states. California is NOT one of them (no state estate tax), but New York, Massachusetts, Washington, Oregon, and others have state-level estate taxes with much lower exemptions ($1M-$7M).

The 199A QBI permanence — for retirees with side income

Section 199A (the 20% qualified business income deduction) was scheduled to sunset after 2025. OBBBA made it permanent.

For retirees, this matters in several common scenarios:

- Consulting income in semi-retirement — Schedule C self-employment income qualifies if the activity isn't a "Specified Service Trade or Business" (SSTB), with phase-out rules above $394K MFJ taxable income.

- Rental real estate — qualifies under the Section 199A Safe Harbor (Rev. Proc. 2019-38) if you meet specific requirements (250 hours of rental services, separate books, etc.).

- Royalties — qualify if they're from a qualified trade or business in which you were actively engaged.

- Board fees, advisory income, expert witness fees — typically qualify as consulting income (subject to SSTB rules if applicable).

For a retiree with $50K of qualifying QBI from consulting, the 20% deduction is $10K of federal taxable income removed. At the 22% bracket, that's $2,200 of federal tax saved annually. Made permanent by OBBBA, this is a recurring benefit for retirees with any pass-through income — not a temporary windfall.

How OBBBA interacts with retirement planning

Three planning implications worth thinking about:

1. Roth conversion math is mostly unchanged, but timing matters

The permanence of the TCJA brackets means you no longer have a 2025-sunset urgency to convert. You CAN take a more measured pace. BUT — the senior bonus deduction phase-out at $150K-$250K MAGI creates a new "donut hole" where the effective marginal rate is meaningfully higher than the bracket rate. Conversions sized to stay under $150K MAGI capture maximum advantage. Conversions in the $150K-$250K range pay an extra ~5% effective rate due to the phase-out.

2. Itemize-vs-standard recalculation

The expanded SALT cap, plus the senior bonus deduction, materially change the itemize-vs-standard breakpoint. Many retirees who haven't itemized since 2018 should re-run the math each year through 2029. Charitable bunching strategies become more powerful.

3. Estate planning becomes income-tax planning

The $30M MFJ federal estate exemption removes estate tax for virtually all families. Estate planning attention shifts to income tax mechanics: which assets receive step-up basis, which trigger inherited-IRA 10-year drain, which preserve QBI treatment for heirs, and so on.

The workshop linked below walks through the new OBBBA-era retirement planning framework with specific worked examples.

Free workshop — 2026 Retirement Tax Strategy Under OBBBA

Hans walks through how the senior bonus deduction, SALT cap, and permanent TCJA brackets change the math in his SoCal workshops.

See Upcoming Workshops